Open Banking

and Open Finance

Open banking and open finance will change and have a lasting impact on the banking industry. The Swiss Bankers Association recognises the significant potential for the financial centre. It considers market-based solutions as key to maintaining the trust of customers.

Potential for all market participants

Changing customer needs, new stakeholders and innovative technologies are posing challenges for traditional banks. In light of the increasingly fragmented value chain, where customers are being served by a large number of different financial services providers such as banks, fintech companies and providers from other industries, it is no longer a question of whether open banking and open finance will establish themselves, but in what form.

The Swiss Bankers Association is closely monitoring this process. It recognises the significant potential of open banking / open finance for all market participants, and is therefore actively contributing to the establishment of framework conditions that facilitate the corresponding business models and thus increase the competitiveness of Switzerland’s financial centre.

Trust especially important

The Swiss Bankers Association recognises the opportunities that arise from opening interfaces and collaborating with third parties. However, it is crucial that this opening is not just one-sided. The mutual exchange of data provides added value to all stakeholders – customers, third-party providers and banks.

The opening of interfaces and increased data exchange also give rise to new challenges, especially in the area of data protection and cyber security. For Swiss banks, the protection of customer data is fundamental. Data exchange must therefore take place at the highest technical level, which must be ensured not only by the banks involved, but also by the third-party providers.

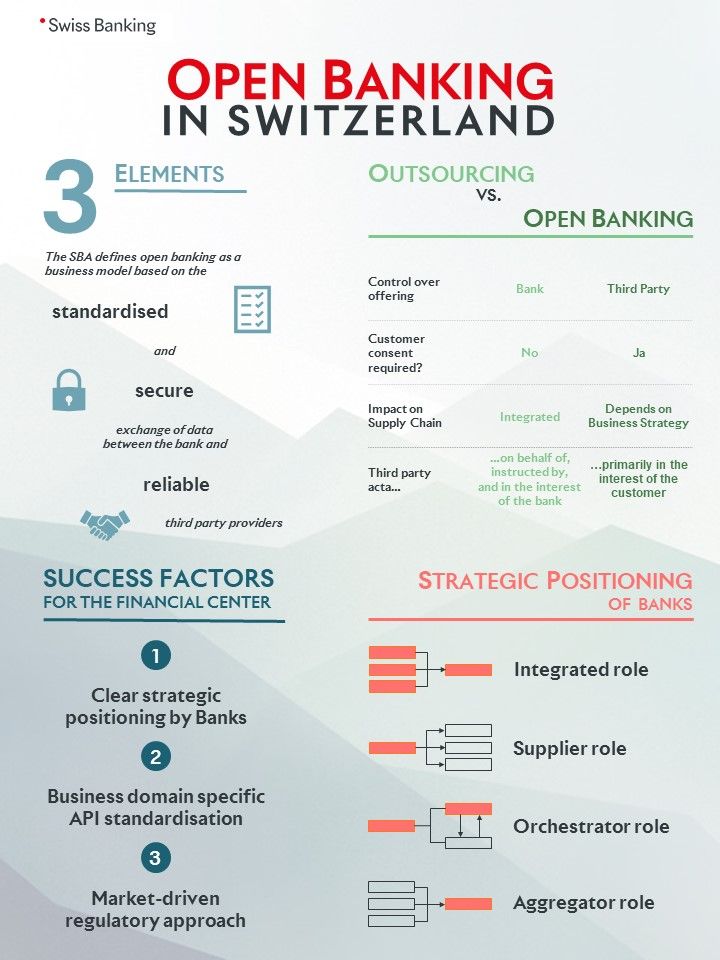

The SBA defines open banking as a business model based on the standardised and secure exchange of data between the bank and reliable third party providers, which can also be other financial services providers.

- “Standardised”: Open standardisation of interfaces is a prerequisite for seamless third party docking and error-free data exchange. The standardisation of interfaces should to the greatest extent possible be based on recognised market standards.

- “Secure”: Ensuring data confidentiality and security requires technological safeguards.

- “Reliable”: The maintenance of system integrity requires that third parties are only granted access to the interface if they meet certain quality criteria – in particular, the highest technical requirements. The decision to share a customer’s data is always made by the customer itself. With an appropriate offering from third party providers, the bank positions itself as a reliable partner and protects the interests of its customers. In doing so, every bank contributes to the security and stability of the Swiss financial centre and underscores why customers should continue to place a high level of trust in Swiss banks in the future.

{kind=link}

Multibanking allows bank customers to manage accounts with multiple banks via a single platform. Technically, it is an open banking use case in which application programming interfaces (APIs) are used to efficiently merge data from different institutions. The activated functions vary depending on the scope of a particular multibanking solution. These functions include, for example, accessing information on account balances and transactions, submitting payments for approval, and directly triggering payment instructions from third-party accounts. This helps customers keep track of their finances, but also makes transactions faster and simpler to execute.

Multibanking solutions for corporate customers based on established standards such as EBICS and SWIFT have been around for many years. While these solutions may work well for the corporate segment, they are not sufficiently user-friendly to appeal broadly to private customers, and so have not yet made the breakthrough into that segment in Switzerland.

Due to recent efforts on standardising API specifications (e.g. SFTI’s Common API) and various API platforms, multibanking is now feasible as an offering for private customers too. One unresolved issue is the potential lack of acceptance of initiatives by banks and other companies, for whom it only makes sense to invest in new multibanking solutions if other relevant players are also offering open APIs at the same time. The memorandum of understanding published by the SBA in May 2023 actively addresses and aims to overcome this challenge.

Shared understanding of roles

The SBA and Swiss Fintech Innovations (SFTI) have worked with all the relevant financial centre stakeholders to agree on the roles each will play in future cooperation on open banking / open finance, particularly in terms of API standardisation. SFTI is acting as a central forum, drawing up the necessary business and technical principles and recommendations for open banking / open finance in Switzerland in conjunction with leading national and international stakeholder groups and partner organisations. Its working group is broad-based, bringing together representatives of banks and insurers as well as fintech and technology firms. The SBA, for its part, is assuming a coordinating role in conveying the industry’s concerns to politicians, authorities and the general public, which it can do in a targeted and effective manner thanks to the clear allocation of roles.

The Swiss Bankers Association’s position

Links & Documents

Overview Open Banking (2020)

Position Paper: Open Banking

Onepager Open Banking

Allocation of roles Open Finance