The OECD’s project for a global minimum tax rate

The OECD has been working for some time on new rules intended to redistribute global tax revenues. These will have an especially severe impact on Switzerland, an export-oriented country with moderate taxation and a small domestic market. The Swiss Bankers Association is committed to preserving the foundations of Switzerland’s success on behalf of its members.

Referendum on amending the Constitution on 18 June 2023

What is the project all about?

The OECD’s project concerns the taxation of the cross-border economic activities of large domestic corporations and domestic branches of large foreign corporations. If a company domiciled in Country A sells its products in Country B, both countries would have good arguments for taxing the profit it makes on these sales. To prevent both countries from taxing the same profit, which would be harmful to both of their economies, it has for a long time been common to sign a double taxation treaty setting out which shares of profit each country is allowed to tax. There are currently just over 3,000 such treaties worldwide, and they are based on international standards to ensure interoperability. The most important standard is that of the OECD, which was originally developed in the 1920s. Back then, it was neither possible nor conceivable for a company to engage in cross-border activities without having a physical presence in another country. As a result, all double taxation treaties have always been based on the idea of a physical presence, be it a factory, a branch, staff, offices etc.

The digital transformation has now made it possible to sell information-based services in particular anywhere in the world without setting foot in another country. Digital technology is able to replace locally based physical activities such as brokerage completely, which has the effect of shifting the taxation of the same economic activity from Country B (where the sales are made) to Country A (where the company is domiciled). The OECD took note of this trend several years ago and has been seeking to modernise its standard for double taxation treaties ever since. However, since we are not really witnessing the emergence of a separate “digital economy” but rather the digitalisation of the economy as a whole, piecemeal changes have proven ineffective. That said, fundamental changes to the standard would drastically alter those 3,000-plus double taxation treaties and thus affect how the global tax “pie” is sliced up. It was thus not long before the focus shifted away from the digital transformation and onto the world’s biggest and most successful companies (Pillar One) while also targeting a global minimum tax rate on corporate profits (Pillar Two). While Pillar One redistributes countries’ taxation rights, therefore, Pillar Two restricts how lenient their taxation can be.

How does the concept work?

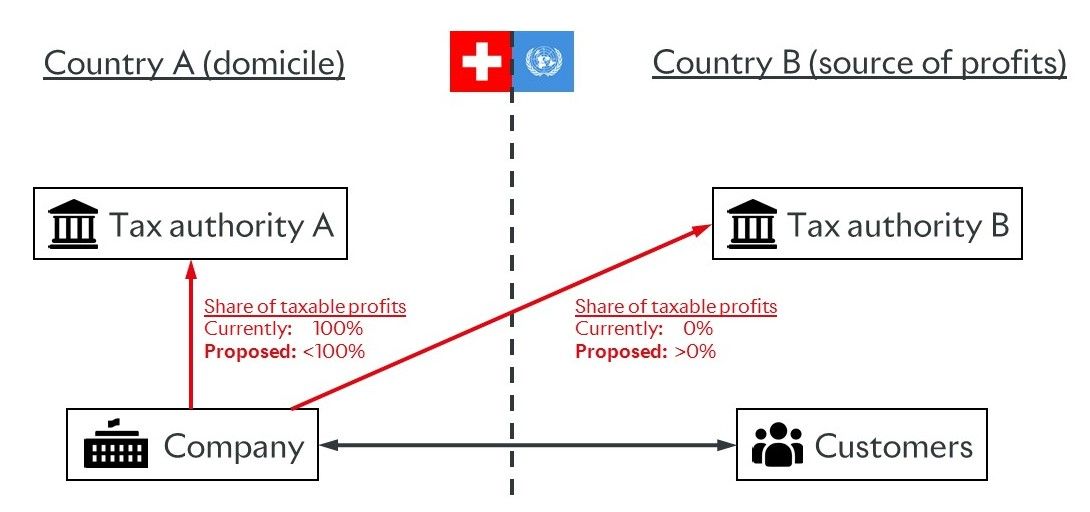

Pillar One

In the initial phase, Pillar One essentially covers the cross-border profits of companies with total revenues of more than EUR 20 billion and a profit margin of more than 10% that are domiciled in Country A and have no physical presence in Country B. Profit generated in Country B has up to now only been subject to taxation in Country A because that is where the (physical) value creation takes place. Under the proposed new rules, Country B would be entitled to tax a share of this profit because the customers are regarded as more important to value creation:

{kind=link}

In simplified terms, the taxable profit in each country would be determined by their respective shares of the company’s sales revenues. From the Swiss perspective, this mechanism theoretically works in both directions: Swiss exporters must pay tax on their profits in other countries, and foreign companies exporting to Switzerland must pay tax here.

A Swiss company with no foreign presence generates a total profit of 300, made up of 100 from sales in Switzerland and 200 from foreign sales. Let us assume that the tax rates are 10% in Switzerland and 20% elsewhere. The amount of tax is currently 30 = 300 x 10%, payable in Switzerland only. Put simply, the proposed rules would require the Swiss company to pay a total of 10 = 100 x 10% in Switzerland and 40 = 200 x 20% elsewhere, equating to 20 = 10 + 40 – 30 more than at present. Meanwhile, a foreign-domiciled company with no presence in Switzerland generates a total profit of 200, made up of 150 from sales in Switzerland and 50 from foreign sales. The foreign company currently pays no tax at all in Switzerland, but the proposed rules would require it to pay 15 = 150 x 10% (together with 10 = 50 x 20% elsewhere). Switzerland would therefore lose out on tax revenues totalling 5 = 10 + 15 – 30, while the Swiss company’s tax burden would rise by 20.

As regulated financial service providers, banks are exempt from Pillar One, as is the mining industry. According to the OECD, there are legal, technical and practical reasons for this exemption. First and foremost, banks are subject to stringent regulation that, in many cases, prevents them from operating any cross-border business without a local presence or at least severely restricts their ability to do so. Regulation also restricts other aspects of banks’ customer acquisition and general operations. The OECD recognised these and other characteristics specific to banking at an early stage and quite rightly worked out an exemption to take account of them. It would not be politically expedient for a country to use supervisory law to restrict foreign banks’ business while also taxing their profits.

Pillar Two

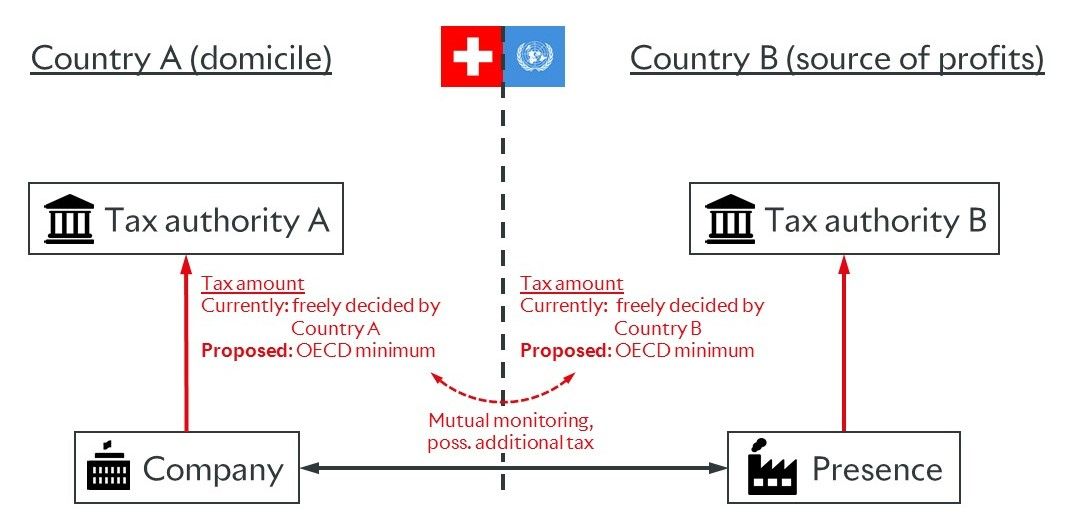

Pillar Two covers the cross-border profits of corporations with total revenues of more than EUR 750 million. In contrast to Pillar One, however, it only includes those with a physical presence (in particular subsidiaries) in the other country. Pillar Two is therefore independent from Pillar One.

The tax a company pays on its profit is currently determined only by the tax rate in its country of domicile. Under the proposed rules, each country where the company makes sales would also be allowed to tax it if – in simplified terms – the taxes paid by certain group entities (e.g. subsidiaries in other countries) on their profits were below an internationally agreed minimum amount.

{kind=link}

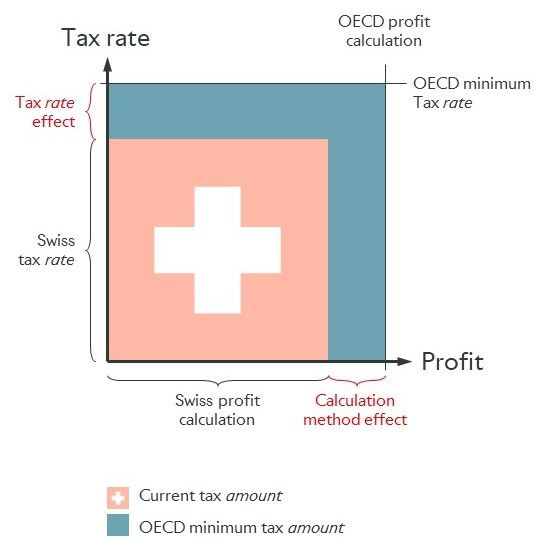

The minimum tax amount would be determined by an international minimum tax rate of 15% on profit calculated in accordance with international accounting principles. In each case, the higher of the two tax amounts (either the normal tax amount in the country of domicile or the OECD minimum tax amount) would apply. The higher amount would thus always be payable, regardless of where. From the Swiss perspective, this mechanism also theoretically works in both directions: Swiss companies with a presence in high-tax countries would have to pay more tax on their profits, while foreign companies from low-tax countries with a presence in Switzerland would also have to pay more.

What impact will this have?

Switzerland is an especially vulnerable net loser under the proposed OECD standard. While Pillar One theoretically works in both directions, the reality is that Switzerland exports far more than it imports. It is an attractive base for a wide range of industries, but its domestic market is very small. This combination clearly sets it apart from other low-tax countries, which are the real focus of the OECD’s project. Pillar Two also theoretically works in both directions, i.e. all low-tax countries would have to raise their tax rates in line with the OECD minimum. In practice, however, Switzerland’s moderate tax levels by international standards mean that it does a great deal more business with high-tax countries than with those where taxes are lower. It would thus lose more as a result of its reduced appeal for these high-tax countries than it would gain from the low-tax countries. The two pillars together would erode Switzerland’s tax base in favour of other countries while also being detrimental to its international competitiveness. The cost of basing a business in Switzerland would rise, and with it the pressure on Swiss wages. The OECD project could therefore have an impact not only on Swiss incomes but also on the welfare mechanisms that depend on them, including pension funds and social security. As regards Pillar Two, this can only be mitigated by Switzerland raising its tax rate for the companies concerned to the OECD minimum and thus at least preventing the difference from flowing to other countries and allowing it to be invested in efforts to improve competitiveness. International competition among business locations will continue, and even though it is set to be restricted in terms of taxation, it can be expected to intensify in other areas.

How does it affect Swiss banks?

As regulated financial service providers, banks are exempt from Pillar One, as is the mining industry. However, banks reflect the overall economy and would therefore be indirectly affected if Switzerland’s competitiveness were to be diminished. In Pillar Two, Switzerland’s large and foreign banks (but not small and medium-sized institutions) would in principle be affected just as much as other Swiss-based large and foreign companies. There are also certain aspects particular to the banking business that would be especially affected by Pillar Two, one example being the significant differences between the way in which earnings are calculated in Switzerland and internationally. Under the system proposed by the OECD, the higher of the two annual profit values would always be taxed, so normal fluctuations in value from year to year could result in the same amount being taxed twice. It will be essential to find solutions in the calculation methodology that can counteract these effects.

The banks are neither the motivation behind nor the focus of the minimum tax project, but they will be subject to substantially higher taxation for the reasons outlined above. This affects only book profits, which are not the result of higher value creation. Even the OECD itself admits that this is not its intention. While this is also a problem in other sectors, the financial industry in particular sees itself faced with an unnecessary, avoidable and disproportionate tax burden. The banks are therefore advocating for the minimum tax rate to be implemented as precisely as possible for the benefit of the entire Swiss economy.

What is Switzerland doing?

In view of its high dependence on international business, Switzerland feared economically harmful double taxation as a result of other countries making unilateral decisions on tax. It therefore agreed to the initiative, subject to certain conditions, in summer 2021 in the interest of legal certainty. Switzerland expressly calls for the rules to take due account of the interests of small, innovative countries and for national legislative procedures to be respected in their implementation. It also wants the new rules to be implemented uniformly by all member states and a solution to be found that balances the minimum tax rate and the calculation method. To this end, Switzerland has chosen a staggered implementation procedure that is appropriately geared to the project’s ambitious timetable and its complexity.

The banking industry, working with the rest of the Swiss economy, supports the decision, the implementation plan and the Swiss conditions in spite of its concerns, but it also sees the said conditions as a yardstick for national implementation. The top priorities for the banks in Switzerland are legal certainty through international acceptance as well as implementation and compliance costs in view of the project’s highly complex nature. However, these priorities cannot justify the expected additional burden, nor can they compensate for it. It remains a de facto tax hike. With this in mind, the banks, which will pay more under the minimum tax rate regardless of what happens, are in favour of securing Swiss tax revenues, first and foremost because they have a clear expectation that this additional tax will be used (within the constraints of international acceptance) to help the companies placed at a competitive disadvantage.

Q&A

Companies compare overall costs when choosing a country as their base. Corporate taxes and personnel costs make up a large share of these, and they also influence each other. If a country’s corporate taxes rise, its overall costs become less competitive internationally, which in turn puts pressure on personnel costs.

No. The focus is no longer on the “digital economy” but instead on the digitalised overall economy, all sectors included. Switzerland could indeed benefit from Pillar One insofar as foreign companies’ Swiss profits would be taxed in Switzerland. However, this gain would be offset by the loss resulting from Swiss exporters having to pay tax on their foreign profits. Since Switzerland exports more than it imports, it would still be a net loser on the basis of Pillar One. As far as Pillar Two is concerned, Switzerland could benefit from low-tax countries having to raise their tax rates, but this gain would be offset by the tax revenues lost to high-tax countries. Since it does far more business with the latter, Switzerland would also be a net loser on the basis of Pillar Two.

Pillar Two actually requires a minimum tax amount, which is determined by applying the international minimum tax rate to the profit calculated according to international accounting principles. Even if the minimum tax rate is equal to or even lower than the Swiss rate, there are significant differences between the methods used to calculate profits in Switzerland and internationally that could more than offset the tax rate effect.

{kind=link}

Temporary differences could lead to double taxation (see above). Permanent differences would almost certainly lead to higher taxation.

Yes, and these are set to take on greater importance. However, limiting competition over the taxation of corporate profits will significantly weaken a key advantage that has hitherto been especially beneficial to Swiss incomes. Just as lowering the tax rate by one percentage point has in the past created large numbers of highly paid jobs, raising it by one percentage point could jeopardise these same jobs. This is all the more important because Swiss companies are so sensitive to tax hikes on account of the country’s tradition of moderate taxation. For these reasons, we need to put a lot of effort into preserving Switzerland’s competitiveness in terms of taxes.

Yes. The very fact that Switzerland is unique in having attracted so many large and foreign corporations and that premium products from Switzerland are in demand all over the world is what makes it so exposed. Moreover, large corporations act as a key multiplier for the local economy, and there is always potential for foreign firms to choose Switzerland as the location of their head office. Taken together, these two factors are Switzerland’s gateway to the global marketplace. Given its modest size and high dependence on the global economy, large and foreign corporations are much more important to Switzerland than they are to countries with large domestic markets.

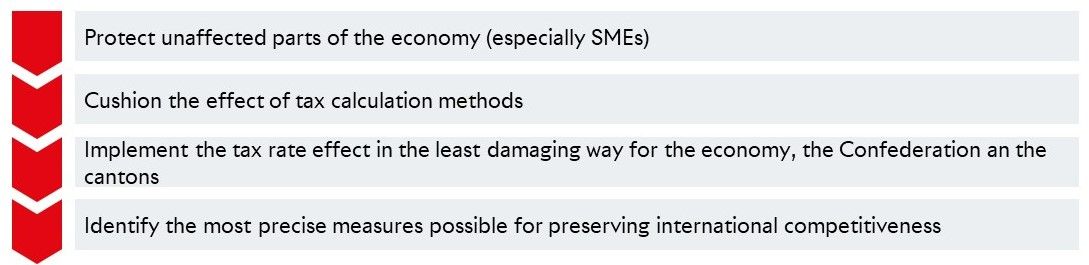

The Swiss Bankers Association is supporting efforts to clarify the technical aspects for the Swiss economy as a whole in conjunction with the federal and cantonal governments and academics. The aim is to formulate proposals for how Switzerland could implement the OECD requirements in an internationally acceptable manner while keeping the negative impact on its appeal as a business location to a minimum. The focus here is on Pillar Two.

{kind=link}

The SBA is concentrating on the effect of tax calculation methods and measures to preserve Switzerland’s international competitiveness. Switzerland must approach this fresh challenge with its usual confidence, creativity and flair for carving out its own niche, since international competition will remain as tough as ever.