COVID-19 loans mainly granted to small enterprises

Social bookmarks

Over eight out of ten Swiss francs loaned were granted to microenterprises and small Swiss companies

47% of the total loan volume – and thus about half of the COVID-19 loans – were granted to microenterprises with up to ten employees, while 35.7% of the loan volume was granted to small enterprises with 10 to 49 employees. Overall, more than eight out of ten Swiss francs granted through the loan programme therefore went to micro and small enterprises.

Big banks and cantonal banks account for 70% of the lending volume

According to SECO, 123 banks are participating in the SME loan programme. The difference in the size, regional distribution and business models of these banks is significant. For example, PostFinance, which does not normally grant loans, is also participating in the programme. The overwhelming majority of banks with a lending business is therefore now supporting their corporate clients through bridging loans.

In terms of lending volumes, the big banks have granted around 40% of all COVID-19 loans, and the cantonal banks over 30%. The Raiffeisen banks and other banks accounted for over 12% of the volume, while around 5% is attributable to PostFinance.

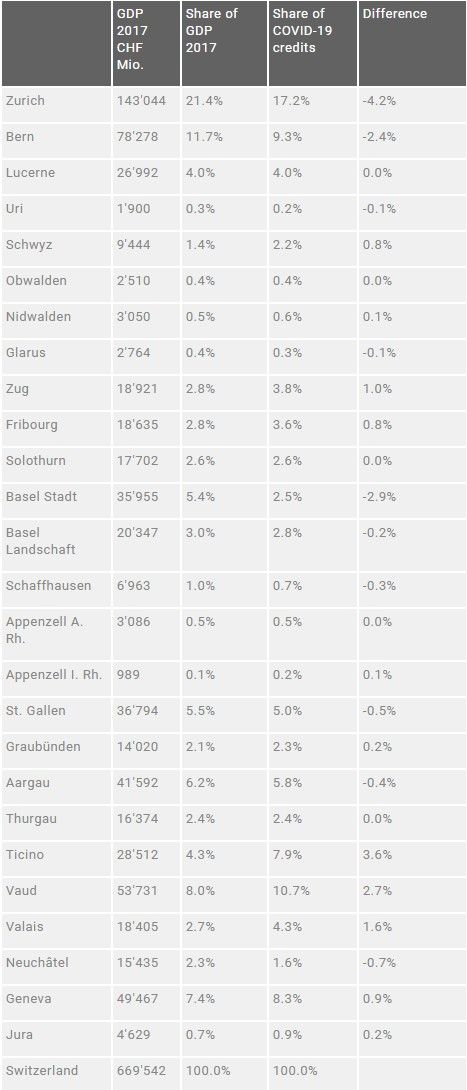

Ticino, Vaud, Valais and Zug with proportionally highest shares

Not surprisingly, the majority of COVID-19 loans were granted to SMEs based in the largest cantons, i.e. Zurich, Vaud, Bern and Geneva.

A more concrete overview can be obtained by comparing the share of bridging loans with the cantons’ gross domestic product (GDP). The most recent figures available to this end are from 2017: compared to GDP, Zurich, Basel-Stadt and Bern received the lowest number of bridge loans and the cantons Ticino, Vaud, Valais and Zug the highest. In the majority of the cantons, however, the share of the COVID-19 lending volume is proportional to cantonal economic output.

The differences that exist are likely on the one hand attributable to the structure of the sectors in the individual cantons. For example, big companies, which in some places contribute a large share to GDP, are excluded from the SME loan programme. On the other hand, the different COVID-19 infection rates in the various cantons likely also played a role. The SME loan programme of the federal government and the banks will remain in place until 31 July 2020.

{kind=link}

Source: covid.easycov.swiss, Seco, Federal Statistical Office

Further analyses of the loan allocations as part of the SME loan programme can be found on the SECO website.